Indian MSMEs are the backbone of India’s growth story, but many still struggle every month to keep cash flowing smoothly for salaries, stock, rent, and new orders. The gap between money going out and customer payments coming in creates constant pressure, and traditional bank loans alone are no longer enough to bridge this gap. That is where smart, flexible MSME working capital solutions combining bank products, government support, and new‑age fintech come into play.

What Are MSME Working Capital Solutions?

MSME working capital solutions are financial tools that help small and medium businesses manage day‑to‑day cash needs like buying raw materials, paying staff, or handling utility bills. Instead of waiting for customers or large buyers to pay on time, MSMEs can tap into short‑term funds to keep operations stable. Businesses can also fast-track your working capital cycle with invoice discounting at Growmax, unlocking funds from approved invoices without adding long-term debt.

These solutions can include:

- Bank overdrafts and cash credit limits

- Short‑term working capital loans

- Invoice and bill discounting on approved invoices

- Supply chain finance and vendor funding

- Fintech‑driven revenue‑based or cash flow‑linked lending

The goal is simple: ensure that a viable business never has to stop production or miss opportunities just because cash is stuck in receivables.

Why Working Capital Matters for MSMEs in India

MSMEs contribute over a quarter of India’s GDP and employ millions, yet a large percentage still operates with thin margins and limited reserves. Delayed payments from large buyers, seasonal demand changes, and rising input costs can quickly create stress on cash flow.

When working capital is tight, MSMEs may:

- Delay supplier payments and lose credit terms

- Cut back on production even when there is demand

- Miss bulk‑purchase discounts on raw materials

- Struggle to pay staff on time and retain talent

Strong, reliable working capital finance for MSMEs gives owners confidence to accept bigger orders, explore new markets, and negotiate better deals with suppliers.

How MSME Working Capital Solutions Work

Most MSME working capital solutions are structured as short‑tenor funding linked to business activity, not long‑term assets.

In simple terms, the process usually follows these steps:

- The MSME identifies a cash gap – upcoming expenses versus expected inflows.

- It chooses a suitable solution – bank loan, overdraft, invoice discounting, or a fintech‑based product.

- Lenders assess the business using documents, bank statements, GST data, or invoice details.

- A working capital limit or one‑time facility is approved.

- The MSME draws funds as needed and repays from customer payments or ongoing revenue.

This cycle can repeat many times in a year, helping MSMEs smooth out ups and downs in cash flow without constantly reapplying for new long‑term loans.

Traditional Bank Loans vs Modern Working Capital Finance

Banks have long been the main source of working capital finance for MSMEs in India, through overdrafts, cash credit, and term loans. These products are reliable but often have strict collateral requirements, lengthy paperwork, and slower turnaround times.

Modern options are changing this picture:

- Invoice discounting and bill discounting on TReDS platforms

- Supply chain finance programs driven by large anchor buyers

- Fintech‑powered revolving credit lines based on cash flow data

- Digital merchant loans linked to POS or online sales

These evolving models align closely with supply chain finance strategies for IndianPixel SMEs strengthening vendor relationships & cash flow, helping businesses maintain trust with suppliers while ensuring smoother liquidity. Instead of relying only on past financial statements or property as security, newer models evaluate live business data to decide eligibility and limits.

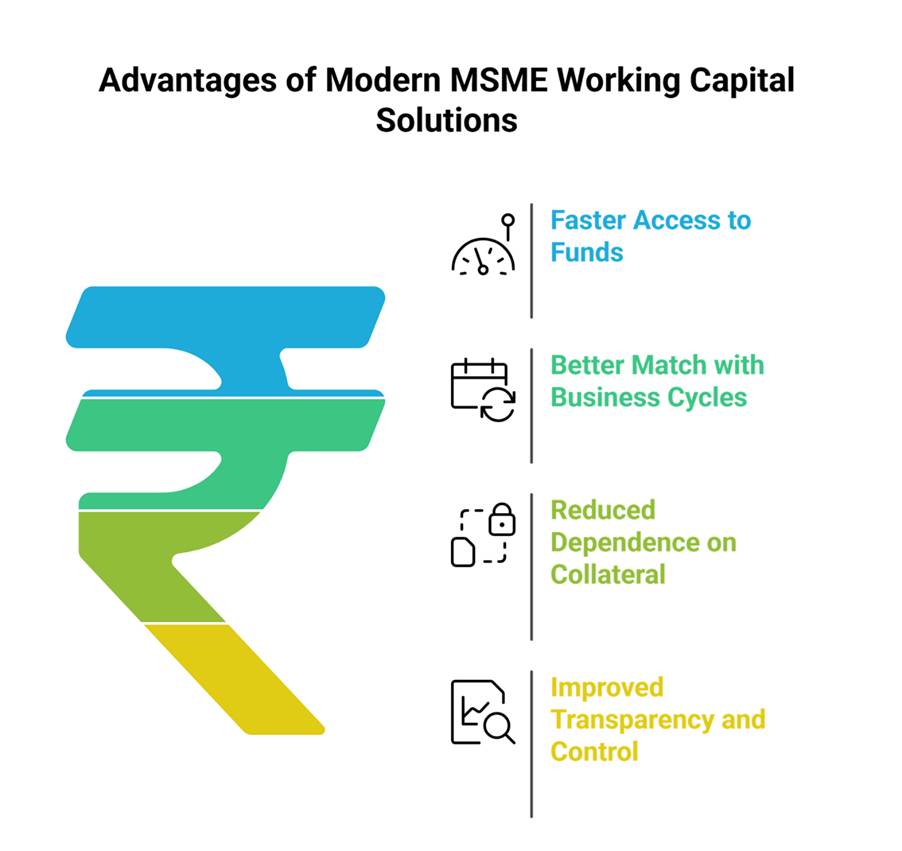

Key Benefits of Modern MSME Working Capital Solutions

When MSMEs combine bank products with digital and fintech options, they gain multiple advantages.

Faster access to funds

- Digital journeys reduce branch visits and manual paperwork.

- Some fintech lenders approve and disburse funds in days or even hours.

Better match with business cycles

- Limits can be linked to invoices, sales, or buyer programs.

- MSMEs can draw funds when needed and avoid paying for idle limits.

Reduced dependence on collateral

- Alternative credit models use invoices, buyer strength, or transaction data instead of only property.

- This helps younger businesses with limited assets get a fair chance at credit.

Improved transparency and control

- Dashboards and platforms show live status of limits, dues, and upcoming payments.

- Owners can plan working capital more proactively instead of reacting to crises.

Types of MSME Working Capital Solutions in India

Different businesses need different blends of funding. Below are the main categories of MSME working capital solutions used today.

1. Bank Overdrafts and Cash Credit

These are flexible limits where MSMEs can withdraw more than the balance in their current account up to an approved limit.

- Secured against stock, receivables, or property

- Interest charged on the amount used, not the full limit

- Suitable for ongoing, general working capital needs

Understanding and decoding working-capital risk through best practices for MSMEs in India is essential while using such facilities, as proper planning helps avoid overutilization and ensures healthy cash flow management.

2. Working Capital Term Loans

These are fixed‑amount loans designed specifically to meet operating expenses over a short period.

- Repaid in EMIs within a defined tenure

- Useful for short‑term gaps, seasonal stocking, or one‑time working capital boosts

3. Invoice and Bill Discounting

Under invoice discounting, MSMEs get paid early against approved invoices raised on credible buyers.

- Funds can arrive within 24–72 hours of invoice approval

- Particularly useful where buyer payment cycles stretch to 60–120 days

- Available via banks, NBFCs, and regulated digital platforms

4. Supply Chain Finance

Supply chain finance programs are built around large anchor corporates and their vendor or dealer networks.

- Vendors can receive early payments at competitive rates

- Dealers can access inventory funding to stock more goods

- Risk is often assessed based on the strength of the anchor buyer

5. Government‑linked Schemes

Government schemes provide partial guarantees or subsidised funding to improve access to working capital finance for MSMEs.

- Credit guarantee schemes for collateral‑light loans

- Special lines for export‑oriented or priority sectors

- Programs routed through banks and financial institutions

6. Fintech‑Based Revenue and Cash Flow Lending

New‑age lenders blend technology, data, and flexible structures to offer tailored fintech business loans in india.

- Credit limits based on GST, bank statements, POS, or platform sales

- Dynamic repayment linked to revenue cycles

- Often fully digital, from application to disbursal

Common Challenges MSMEs Face While Accessing Working Capital

Despite many options, MSMEs still face real hurdles when trying to use MSME working capital solutions effectively.

Documentation and compliance overload

- Multiple financials, tax returns, projections, and collateral papers

- Many smaller businesses are not fully organised or formalised

Collateral constraints

- Lack of property or unencumbered assets

- Lower valuations than expected, reducing eligible limits

Limited awareness of new options

- Many owners still think in terms of only term loans or overdrafts

- Low awareness of invoice discounting, TReDS, or digital fintech business loans in india

Fear of complexity and hidden charges

- Confusion over fees, discount rates, processing charges, and penalties

- Worry about over‑borrowing or falling into a debt trap

Best Practices for Choosing the Right Working Capital Solution

Selecting the right mix of MSME working capital solutions is partly about numbers and partly about business behaviour.

1. Map your cash flow clearly

- List your fixed monthly expenses and variable costs.

- Understand your average collection period from customers.

- Identify peak seasons and lean months.

2. Match products to use cases

- Use overdrafts or cash credit for ongoing operational needs.

- Use invoice or bill discounting for large, credit‑period‑heavy customers.

- Use short‑term working capital loans for seasonal stocking or expansion.

3. Compare cost beyond just interest rate

- Look at processing fees, documentation charges, and other add‑ons.

- Check pre‑payment rules, penalty structures, and hidden conditions.

4. Balance bank stability with fintech speed

- Maintain strong relationships with 1–2 banks for long‑term support.

- Use reputable fintech partners for flexibility and speed where it makes sense.

How Fintech Is Changing Business Loans in India

The landscape of fintech business loans in india is expanding rapidly, giving MSMEs more choice than ever before.

Key shifts include:

- Use of AI and alternative data for faster, more accurate credit assessment

- End‑to‑end digital journeys with video KYC and e‑signatures

- Products tailored to specific sectors (manufacturing, services, exporters, D2C, traders)

- Embedded finance built into accounting software, marketplaces, and payment platforms

For MSMEs, this means shorter waiting times, better‑matched products, and the chance to build a credit history through digital transactions.

Implementation Roadmap: Moving from Bank‑Only to Blended Working Capital

To make full use of modern MSME working capital solutions, MSMEs can follow a practical roadmap.

- Audit your current funding mix

a. How much comes from bank limits, trade credit, promoter funds, and informal sources? - Identify key pain points

a. Are delays from a few large customers hurting you?

b. Do you struggle during specific months or seasons? - Explore targeted solutions

a. Invoice discounting for delayed receivables

b. Supply chain finance if you work with large anchor buyers

c. Digital working capital limits for quick, smaller top‑ups - Formalise business data

a. Maintain clean GST filings and financial statements.

b. Use digital payments and banking for stronger transaction trails. - Partner with a trusted platform

a. Choose partners that specialise in working capital finance for MSMEs, not just any generic loan.

Example Scenarios: How MSMEs Use Modern Working Capital

Manufacturing unit with long receivables

A small auto‑component manufacturer supplies to large OEMs on 60‑day credit. Instead of taking a bigger term loan, it uses invoice discounting on approved invoices to get funds within a few days, and repays when OEMs clear invoices. This approach allows the business to access invoice discounting solutions and explore MSME-focused funding options that reduce pressure on cash flow without increasing long-term debt.

Distributor needing more stock before festive season

A regional distributor works with a large consumer brand. Using supply chain finance linked to the anchor, the distributor gets dealer finance at better rates and stocks more inventory during the festive rush, increasing sales.

Online D2C brand with fast growth

A D2C brand selling online sees sales doubling each quarter but struggles with marketing and inventory spends. By using a fintech line of credit linked to sales data, it gets short‑term working capital that scales with revenue.

These scenarios show how MSME working capital solutions can be tailored to the business model, not forced into a one‑size‑fits‑all loan.

Future Trends in MSME Working Capital Finance

The next few years will bring deeper integration of technology, regulation, and data into working capital finance for MSMEs.

Emerging trends include:

- Wider use of account aggregator frameworks to securely share financial data

- Greater adoption of TReDS and invoice‑based financing even among smaller MSMEs

- Sector‑specific scoring models for exporters, agri‑processors, and digital‑first businesses

- Stronger partnerships between banks and fintechs to combine low‑cost capital with smart underwriting

These changes aim to close India’s large MSME credit gap while keeping risk manageable for lenders.

How Growmax Empowers MSME Working Capital solutions

At Growmax, the focus is on making MSME working capital solutions practical, flexible, and easy to use for real businesses, not just large enterprises. Growmax connects MSMEs with smarter invoice‑based funding and curated fintech options so owners can spend more time on growth and less on chasing cash. Recent discussions around MSME working capital access, with stakeholders of TReDS-anchored liquidity calling it a structural shift in the Budget, further highlight the importance of technology-driven funding ecosystems for small businesses.

Growmax is a strong partner for your working capital needs because it offers:

- Solutions tailored to MSMEs rather than generic one‑size‑fits‑all loans

- Faster, digital journeys that cut down paperwork and wait times

- Access to partner lenders and curated fintech business loans in india aligned with your business model

- Support that helps you understand and choose the right mix of funding options

If you are looking to stabilise cash flow, fund growth, and reduce stress around collections, explore how Growmax can help you design the right MSME working capital solutions for your business and turn your invoices, relationships, and data into a reliable source of ongoing capital.

FAQ: MSME Working Capital Solutions in India

1. What are the most common MSME working capital solutions available today?

They include overdrafts, cash credit, working capital term loans, invoice discounting, supply chain finance, and digital fintech business loans in india, each serving different cash flow needs.

2. How is working capital finance for MSMEs different from a term loan?

Working capital finance focuses on short‑term operational needs and is usually revolving or short‑tenor, while term loans fund long‑term assets like machinery or property.

3. Do all working capital products require collateral?

Not always. Many invoice‑based and fintech products rely on invoices, buyer strength, or transaction data instead of traditional property collateral.

4. Can a small MSME with limited financial history get digital working capital?

Yes, some platforms use GST, bank transactions, or marketplace sales to evaluate eligibility, making newer businesses more credit‑worthy in lenders’ eyes.

5. How can I decide between a bank overdraft and invoice discounting?

Use overdrafts for general ongoing needs and invoice discounting when a few large customers pay late and you want funds against specific invoices.

6. Are fintech business loans in india safe?

Reputable platforms follow regulations, use secure data practices, and partner with regulated lenders, but MSMEs should still review terms, charges, and documentation carefully.

7. What documents are usually needed for working capital finance for MSMEs?

Basic KYC, business registration, bank statements, GST returns, and sometimes financial statements or invoice copies, depending on the product.

8. Can MSMEs combine multiple MSME working capital solutions?

Yes, many businesses blend bank limits, invoice‑based funding, and selective fintech credit to match different needs without over‑relying on a single source.

9. How do interest rates compare between banks and fintech lenders?

Banks may offer lower base rates but require more collateral and paperwork, while fintech lenders may charge slightly higher rates in exchange for speed and flexibility.

10. How can MSMEs avoid over‑borrowing?

By planning cash flows, tracking utilisation regularly, and choosing products that align with real business cycles instead of taking the maximum possible limit.