Indian MSMEs often run into a familiar problem: sales are strong on paper, but cash in the bank is tight. Payments from buyers take time, while salaries, raw materials, rent, and logistics cannot wait. In this gap, a well‑planned MSME working capital loan helps keep operations smooth without depending only on personal savings or informal borrowing. Understanding MSMEs and their access to invoice discounting services can also help businesses unlock funds tied up in unpaid invoices and improve cash flow management.

What Is an MSME Working Capital Loan?

An MSME working capital loan is a short‑term business loan designed to cover daily running expenses, not long‑term assets. It supports:

- Purchase of raw materials and inventory

- Payment of wages, rent, and utilities

- Marketing, logistics, and small operational costs

Banks and NBFCs treat it as working capital finance for MSMEs, focusing on cash flow and turnover rather than only big assets. Limits and interest rates depend on your revenue, banking history, and overall repayment track record.

Types of Bank Working Capital Loans in India

When you approach a lender, you will usually see a few common formats of bank working capital loan in India:

- Overdraft or cash credit linked to your current account

- Short‑tenor working capital term loans with fixed EMIs

- Flexi or revolving facilities you can draw and repay multiple times

Each format suits a different need. Overdrafts help with frequent small gaps, term loans suit planned requirements for a season, and flexi facilities give more control over when and how much you use.

How These Loans Really Work in Daily Business

Once approved, working capital finance for MSMEs becomes a practical tool you can tap whenever cash flow tightens. The role of digital working capital financing in accelerating growth for SMEs in India is becoming increasingly important, as faster approvals and online platforms help businesses access funds when they need them most.

- You get a sanctioned limit or loan amount based on your financials.

- Funds are drawn to pay suppliers, staff, and essential bills.

- Collections from customers are later used to repay EMIs or reduce the overdraft.

Used wisely, an MSME working capital loan acts like a shock absorber during slow collections or busy seasons. It prevents production stops, protects supplier relationships, and keeps your team paid on time.

When Should MSMEs Use Working Capital Loans?

You should actively consider these loans when:

- Orders are growing but you lack cash for raw materials or labour.

- A few large customers take 45–90 days to pay regularly.

- You are entering a peak season and need extra stock.

- You face a temporary cash crunch, but the business is fundamentally strong.

These are classic cases where working capital finance for MSMEs is more suitable than withdrawing personal savings or taking expensive short‑notice credit.

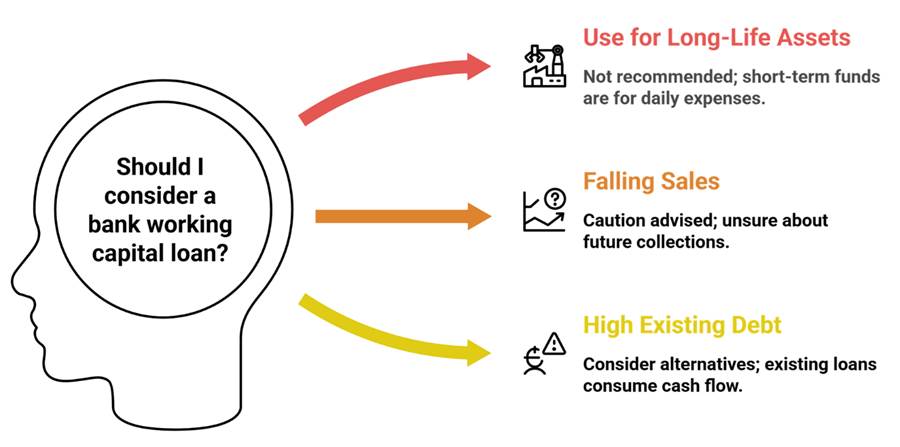

When to Avoid or Re‑Think These Loans

There are times when a bank working capital loan in India may not be the best choice. You should be cautious if:

- You plan to use short‑term funds to buy long‑life assets like property or heavy machines.

- Current sales are falling and you are unsure about future collections.

- Existing loans already take a big share of your monthly cash flow.

In such cases, it is better to first fix the business model, reduce costs, or consider a longer‑tenor term loan before adding more short‑term debt.

Plan Your Next MSME Working Capital Loan Smartly

A well‑structured MSME working capital loan can turn uneven cash flows into steady operations and open doors to bigger orders and new clients. Insights from the analysis of working capital management in Indian MSMEs using secondary evidence show how proper financial planning and efficient cash flow management can significantly strengthen small businesses. Before you apply, map your cash cycle, compare offers from different lenders, and match the loan type with your real‑world need. When chosen and managed with care, this single tool can quietly support your growth, protect your reputation, and make every opportunity easier to accept for your MSME.